Gaston County review will allow time for constructive engagement

BELMONT, N.C. –

Piedmont Lithium Inc. (Nasdaq: PLL) (ASX: PLL) (“Piedmont” or the “Company”) is providing the following update as to the county rezoning process for its Carolina Lithium Project.

On August 6, 2021, during a special meeting of the Gaston County Board of Commissioners, the commissioners voted to approve a 60-day temporary development moratorium in new approvals for mining and quarrying activities in order to review the county’s current industry regulations and their potential impact on future operations. The Company looks forward to constructive engagement with the county commissioners and staff on the many important matters subject to their review.

“We would like to thank the Gaston County Board of Commissioners for their leadership in creating this framework and review structure where the County and Company can move forward together. We wholeheartedly agree that it’s important for the commissioners to have the time to review existing state and county regulations and how they may apply to plans for the Carolina Lithium Project,” said Piedmont Lithium CEO Keith Phillips.

“We note that counsel representing the county made clear in a statement during the special meeting that Gaston County supports economic growth and development, and that the resolution is not intended to stop mining but rather to give the county time to perform their due diligence. We look forward to engaging with the commissioners and the broader community regarding our commitment to environmental stewardship and economic prosperity for the county as we work to advance the United States supply chain for a low-carbon economy.”

Piedmont also confirmed that the Company is on track to publish its upcoming Definitive Feasibility Study in 2H 2021 and the Company will continue to work on the state and county level permits that are required for the Project.

About Piedmont Lithium

Piedmont Lithium (Nasdaq:PLL, ASX:PLL) is developing a world-class integrated lithium business in the United States, enabling the transition to a net zero world and the creation of a clean energy economy in America. Our location in the renowned Carolina Tin Spodumene Belt of North Carolina, the cradle of the lithium industry, positions us to be one of the world’s lowest cost producers of lithium hydroxide, and the most strategically located to serve the fast-growing U.S. electric vehicle supply chain. The unique geographic proximity of our resources, production operations and prospective customers places us on the path to be the most sustainable producer of lithium hydroxide in the world and should allow Piedmont to play a pivotal role in supporting America’s move to the electrification of transportation and energy storage. For more information, please visit www.piedmontlithium.com.

Forward Looking Statements

This press release contains forward-looking statements within the meaning of or as described in securities legislation in the United States and Australia, including statements regarding exploration, development and construction activities; current plans for Piedmont’s mineral and chemical processing projects; strategy; and expectations regarding permitting. Such forward-looking statements involve substantial and known and unknown risks, uncertainties and other risk factors, many of which are beyond our control, and which may cause actual timing of events, results, performance or achievements and other factors to be materially different from the future timing of events, results, performance or achievements expressed or implied by the forward-looking statements. Such risk factors include, among others: (i) that Piedmont will be unable to commercially extract mineral deposits, (ii) that Piedmont’s properties may not contain expected reserves, (iii) risks and hazards inherent in the mining business (including risks inherent in exploring, developing, constructing and operating mining projects, environmental hazards, industrial accidents, weather or geologically related conditions), (iv) uncertainty about Piedmont’s ability to obtain required capital to execute its business plan, (v) Piedmont’s ability to hire and retain required personnel, (vi) changes in the market prices of lithium and lithium products, (vii) changes in technology or the development of substitute products, (viii) the uncertainties inherent in exploratory, developmental and production activities, including risks relating to permitting, zoning and regulatory delays, (ix) uncertainties inherent in the estimation of lithium resources, (x) risks related to competition, (xi) risks related to the information, data and projections related to Sayona Quebec and IronRidge Resources, (xii) occurrences and outcomes of claims, litigation and regulatory actions, investigations and proceedings, (xiii) risks regarding our ability to achieve profitability, enter into and deliver product under supply agreements on favorable terms, our ability to obtain sufficient financing to develop and construct our projects, our ability to comply with governmental regulations and our ability to obtain necessary permits, and (xiv) other uncertainties and risk factors set out in filings made from time to time with the U.S. Securities and Exchange Commission (“SEC”) and the Australian Securities Exchange, including Piedmont’s most recent filings with the SEC. The forward-looking statements, projections and estimates are given only as of the date of this presentation and actual events, results, performance and achievements could vary significantly from the forward-looking statements, projections and estimates presented in this presentation. Readers are cautioned not to put undue reliance on forward-looking statements. Piedmont disclaims any intent or obligation to update publicly such forward-looking statements, projections and estimates, whether as a result of new information, future events or otherwise. Additionally, Piedmont, except as required by applicable law, undertakes no obligation to comment on analyses, expectations or statements made by third parties in respect of Piedmont, its financial or operating results or its securities.

This announcement has been approved for release by the Company’s CEO, Mr. Keith Phillips.

BELMONT, N.C. – Piedmont Lithium Inc. (Nasdaq: PLL) (ASX: PLL) (“Piedmont” or the “Company”) is pleased to provide an update on our recent accomplishments and development plans:

Carolina Lithium Project

Scoping update published in June 2021 contemplating 30,000 tonnes per year (“tpy”) lithium hydroxide production on a single integrated site in Gaston County, North Carolina

Superior sustainability profile vs. current producers in China and South America

Strong projected economics – ~$1.9bb NPV and ~$400mm steady-state EBITDA

Expected to employ ~500 people in well-paying jobs while making Gaston County a magnet for other businesses in the EV supply chain, and driving opportunities for a broad array of local small businesses

Definitive feasibility study expected in the second half of 2021

Permitting and approval process advancing

Clean Water Act Section 404 Standard Individual Permit received in 2019

Will apply for new air permit given the shift to a single site and the Metso Outotec process

Local approval process commenced in July 2021

North Carolina state mining permit application to be submitted in August 2021

Strategic Initiatives

Canada – Sayona Quebec and North American Lithium (“NAL”)

Piedmont owns a 39.6% effective economic interest in Sayona Quebec

Sayona Quebec is poised to become Canada’s largest lithium project by resource tonnage with the completion of the acquisition of North American Lithium expected in August 2021

Ghana – IronRidge Resources (“IRR”)

Piedmont is acquiring a 9.5% stake in IronRidge Resources (AIM: IRR) and may earn up to a 50% interest in IRR’s Ghanaian lithium portfolio

The Ewoyaa project is expected to have strong economics given its high-grade mineral resource, DMS-only process, low-cost hydro power, and close proximity to an international port

Piedmont has offtake agreements in place for 50% of spodumene concentrate production from Sayona/NAL and IRR Ghana, underpinning potential future growth in lithium hydroxide production

Corporate Matters

Piedmont redomiciled to become a US corporation in May 2021

Executive team bolstered with senior appointments including COO and CFO

Lithium offtake discussions ongoing with leading participants in the EV supply chain

Strategic partnering process underway and DOE ATVM loan application to be submitted in H2 2021

Cash balance of approximately $143 million as of June 30, 2021

Keith D. Phillips, President and Chief Executive Officer, said, “Piedmont is positioned to become a leading producer of lithium hydroxide while positively impacting the communities in which we operate by creating jobs, attracting other EV supply chain participants, increasing the tax base, and broadly supporting other local small businesses. Through direct investment and contracted offtake, we control a significant quantity of potential spodumene concentrate production in three critical locations. We believe spodumene is the preferred feedstock for the EV supply chain and that ‘owning the resource’ is the key to value creation in the lithium industry. We look forward to constructively engaging in the permitting and approval process for Carolina Lithium and driving further value for our shareholders by advancing the Quebec and Ghana projects toward development decisions.”

Carolina Lithium Project

On June 9, 2021, Piedmont Lithium published a Scoping Study Update which featured plans to construct a 30,000 tpy lithium hydroxide manufacturing business on a single campus in Gaston County, North Carolina.

The proposed Carolina Lithium Project has the potential for exceptional project economics. There are currently no such integrated sites operating anywhere in the world, and the economic and environmental advantages of this strategy are compelling:

Premier location in Gaston County, North Carolina – “the cradle of the lithium business”

Reduction of spodumene concentrate transportation costs and related noise and emissions

On-site solar power to lower costs and reduce reliance on diesel fueled equipment

Potential to co-locate other downstream battery materials / Li-ion battery manufacturing

Creation of approximately 500 manufacturing, engineering, and management jobs

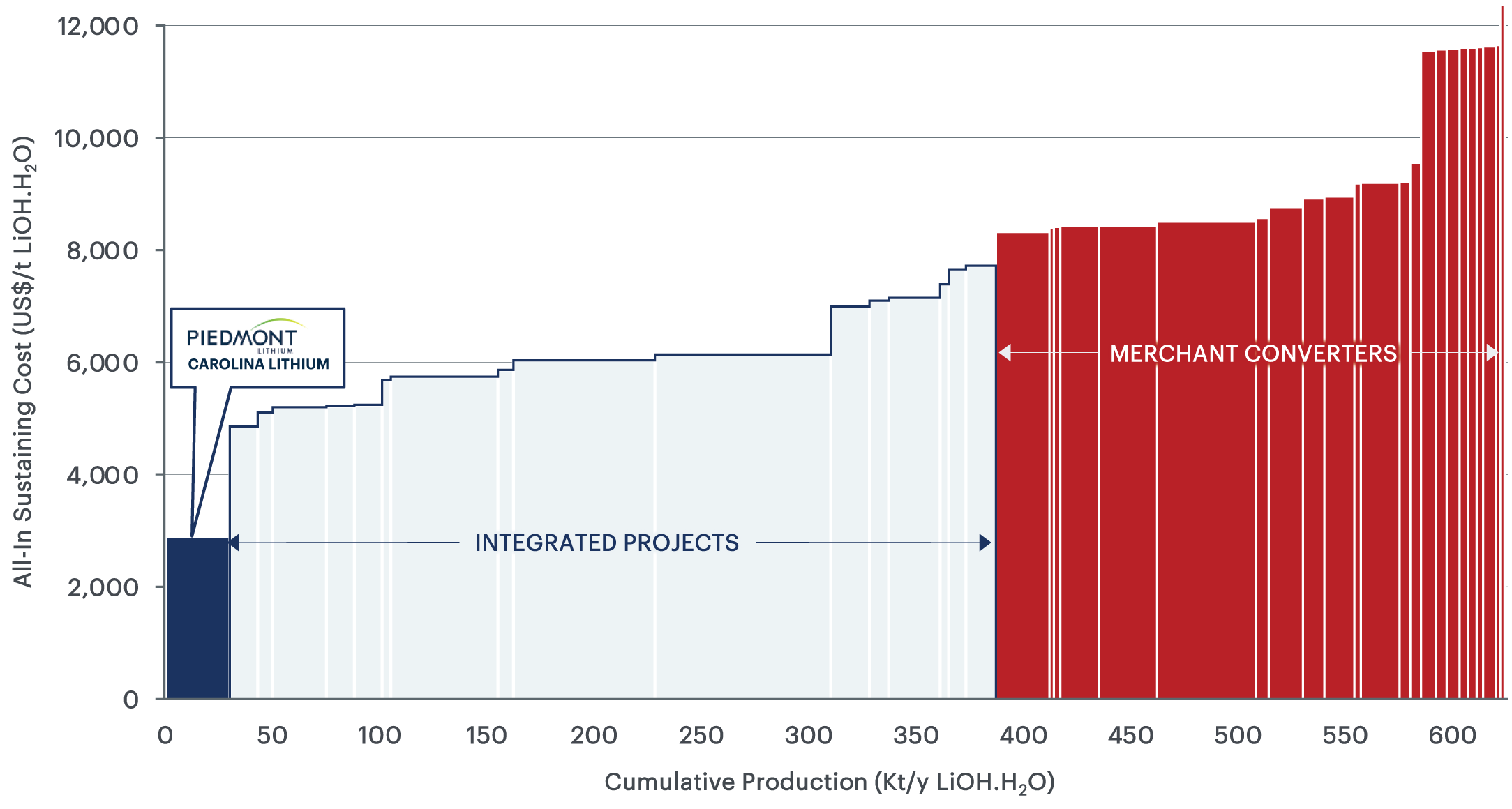

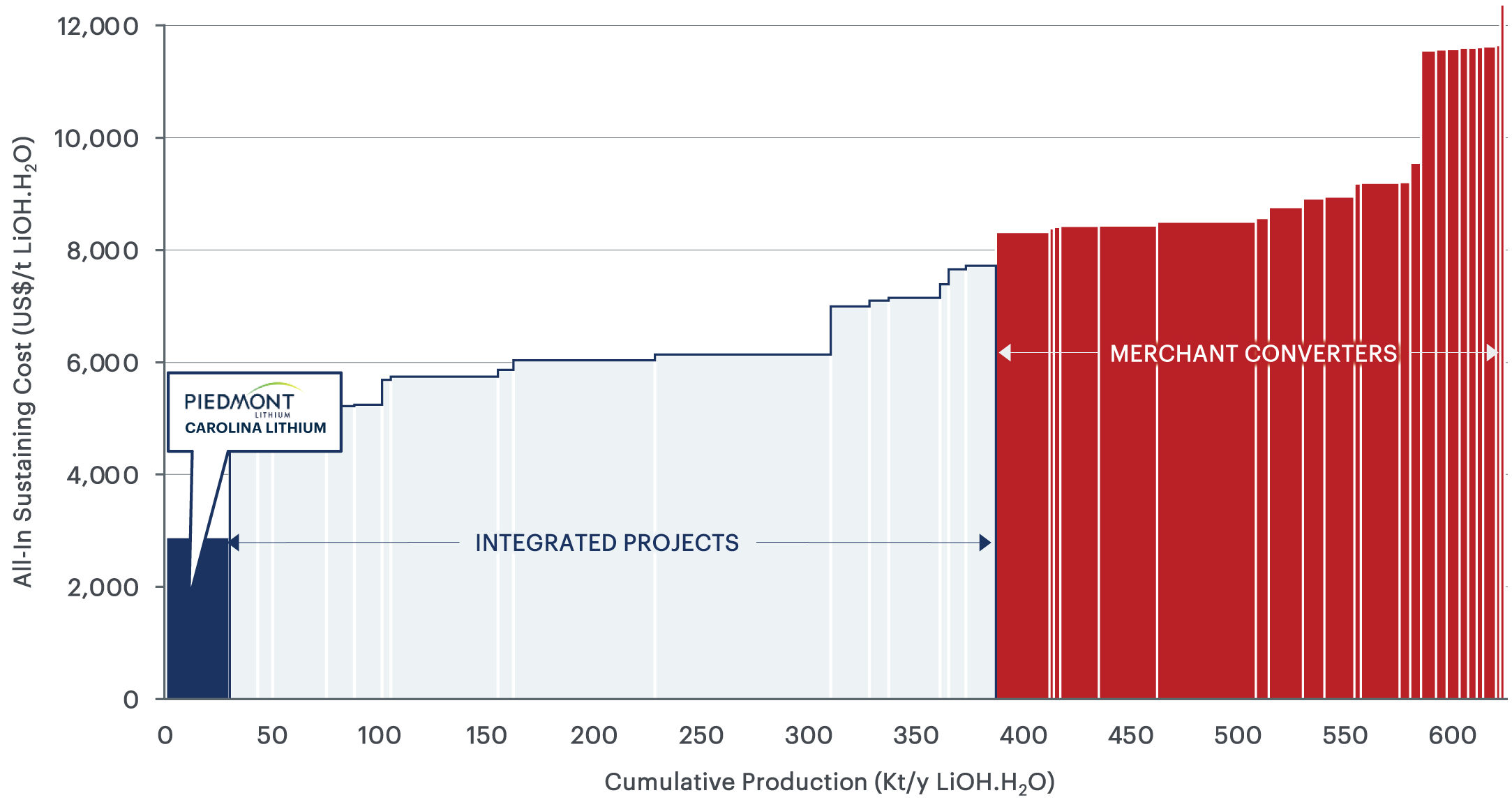

AISC includes all direct and indirect operating costs including feedstock costs (internal AISC), refining, corporate G&A and selling expenses.

Community Impact

Piedmont Lithium expects to employ approximately 500 skilled local workers at an average $90,000 per year in salary and benefits, all in a safe, modern, state-of-the-art work environment.

Our Carolina Lithium Project will make Gaston County a North American leader in the electric vehicle supply chain and attract other supporting businesses that will generate quality jobs and increase tax revenue. Our operation will rely on the support of many small businesses in the area, including maintenance contractors, delivery drivers, caterers, machine shops, fabricators, uniform services, and many more. It will also enable and enrich the base of skilled manufacturing jobs and expand training programs in Gaston County.

Permitting Update

To date, Piedmont Lithium has obtained three important permits required to commence construction of our Carolina Lithium Project, including:

A Section 404 Standard Individual Permit issued by the US Army Corps of Engineers under the Clean Water Act, which included an Environmental Assessment resulting in a Finding of No Significant Impact

An Individual 401 Water Quality Certificate issued by North Carolina Division of Water Resources under the Clean Water Act

A Synthetic Minor Title V Air Permit issued by North Carolina Department of Environmental Quality (“NCDEQ”) – Division of Air Quality under the Clean Air Act

Additional permits or permit amendments will be required before construction can begin on the planned integrated Carolina Lithium operations. Remaining key permits include:

NC State Mining Permit issued by NCDEQ’s Division of Energy, Mineral and Land Resources (“DEMLR”)

Application for a new air permit due to the relocation of Piedmont Lithium’s planned lithium hydroxide manufacturing plant to Gaston County and the switch to the Metso Outotec process

A Conditional District rezoning approval from Gaston County approved by the Gaston County Board of Commissioners

The Company plans to submit its mine permit application to DEMLR in August 2021. After we submit the mine permit application and adjacent property owner notifications have been confirmed, then permit review will proceed through a structured process. This structured process includes a public comment period, review by DEMLR and other state agencies and divisions within NCDEQ, a potential public hearing, possible requests for additional information made by DEMLR, responses by Piedmont Lithium, and issuance of a draft permit.

Conditional district rezoning will require a recommendation by the Gaston County Planning Board and majority approval by the Gaston County Board of Commissioners. Piedmont Lithium expects to conduct multiple public information meetings as part of the rezoning process. The Company made an initial presentation of its integrated project plans to the Gaston County Board of Commissioners on July 20, 2021. The Company is in pre-application consultation with Gaston County at this time and coordinating with county officials with respect to future additional presentation dates.

Each of the DEMLR mine permit and county rezoning approvals will be mutually conditioned upon each other.

Definitive Feasibility Study and Project Timeline

Our Definitive Feasibility Study (“DFS”) of the 30,000 tpy integrated Carolina Lithium Project should be completed within the second half of 2021. The Company currently contemplates a start of construction in Q2 2022 subject to market conditions, project financing, and the successful conclusion of the permitting and approval processes, among other factors.

Canada – Sayona Quebec and North American Lithium

In January 2021, Piedmont Lithium entered into a strategic partnership with Sayona Mining Limited (“Sayona”) (ASX: SYA) through the purchase of an equity stake in Sayona and a 25% interest in its 100%-owned Quebec subsidiary, Sayona Quebec Inc (“Sayona Quebec”). Sayona Quebec owns the DFS-level Authier lithium project and the highly prospective Tansim exploration property, both located near the mining center of Val-d’Or, Quebec.

On June 30, 2021, the Superior Court of Quebec (Commercial Division) granted an approval and vesting order regarding the Company’s joint bid with Sayona for the acquisition of NAL, paving the way for Sayona Quebec to acquire all the shares and substantially all the assets of NAL. The transaction is expected to close in August 2021. NAL owns La Corne, a permitted, brownfield spodumene project located approximately 20 miles from Sayona’s core Authier project. La Corne has a Mineral Resource of 47.0Mt @ 1.19% Li2O[1]and has had over $400 million invested in mining, concentrate and refining capacity. The project was operational and ramping toward nameplate production in 2018, when it was placed on care and maintenance due to weak lithium markets.

The combination of Authier and La Corne will create one of Canada’s largest lithium projects, all strategically located near the mining center of Val-d’Or in the Abitibi region of Quebec, with good proximity to rail and highway transportation networks as well as experienced mining and contracting talent. Piedmont will work closely with Sayona to upgrade the existing spodumene concentrate (“SC6”) plant and integrate the Authier ore body with La Corne. Piedmont has offtake agreements in place allowing the Company to purchase the greater of 113,000 tpy or 50% of annual SC6 production from the merged operation. We are evaluating options to build a conversion operation that could process Sayona SC6 as well as third-party SC6 into lithium hydroxide in Quebec, capitalizing on Quebec’s access to zero-carbon, low-cost hydropower, world-class infrastructure, and the initiative of the Quebec and Canadian governments to develop a local battery materials supply chain.

Mr. Phillips added, “Quebec is poised to become an important lithium production center and Piedmont Lithium is acquiring a significant stake in the province’s largest and best-located spodumene resource. We are developing plans for what could be a world-class Quebec-based lithium hydroxide business to complement our Carolina Lithium strategy.”

Ghana – IronRidge Resources

On July 1, 2021, Piedmont Lithium announced a strategic partnership with IronRidge Resources (AIM: IRR) through the purchase of an equity stake in IRR, staged project investments to earn a 50% interest in IRR’s Ghana-based lithium portfolio (“IRR Ghana”), and a binding supply agreement to purchase 50% of IRR Ghana’s planned SC6 production. IRR Ghana has an impressive portfolio of spodumene prospects, anchored by the highly promising Ewoyaa Project (“Ewoyaa”).

Ewoyaa has a current Mineral Resource of 14.5Mt @ 1.31% Li2O with substantial exploration upside,[2] and we believe it has the potential to be a large, low-cost spodumene concentrate producer. In January 2021, IRR published a scoping study for Ewoyaa forecasting an average of 295,000 tpy of planned SC6 production, a $345 million after-tax net present value and an after-tax internal rate of return of 125%, for initial capital investment of $68 million.[3] These anticipated project economics, if realized, would result in part from Ewoyaa’s location only 70 miles to the major port of Takoradi, direct access to clean solar and hydroelectric power, as well as the DMS-only process which is suitable for Ewoyaa’s coarse-grained spodumene.

Piedmont Lithium hopes to complete a definitive feasibility study for Ewoyaa by mid-2023 and to be producing spodumene concentrate by 2025. Piedmont Lithium believes its Ewoyaa offtake rights can underpin significant growth in its lithium hydroxide position and is currently evaluating possible conversion sites in North America.

“We believe Ewoyaa is an exceptional project with great upside. We believe it is Africa’s best-located lithium project and we look forward to working with our partners at IRR to update the mineral resources and economics at Ewoyaa and incorporate those into our future lithium hydroxide conversion plans in North America,” commented Mr. Phillips.

Corporate Matters

Redomicile – In May 2021, Piedmont successfully completed a redomiciling process to become an American (Delaware) corporation headquartered in Gaston County, North Carolina, with a primary listing on Nasdaq and a secondary listing on the Australian Securities Exchange. The redomiciling process has helped attract U.S. institutional investor and analyst following of the Company, which we believe will drive higher shareholder value over time.

Director and Officer Appointments – As part of our transition to becoming an American company we appointed Claude Demby and Susan Jones to our Board of Directors in May 2021, bringing two seasoned executives with substantial governance experience to help guide our Company. We have added several important members to our team over the past several months, highlighted by the appointments of David Klanecky, former head of Albemarle’s hard rock lithium business, as Chief Operating Officer, and Michael White as our Chief Financial Officer. Piedmont’s employee base is now 24 strong, including a talented technical team with deep experience in the lithium and mining industries.

Financial Position – In March 2021 the Company completed a successful U.S. equity placement and our cash balance was approximately $143 million on June 30, 2021, our fiscal year end. We believe our cash position is sufficient to fund our global pre-construction activities at least through the end of 2022.

Project Financing – In June 2021, we commenced a process to engage with potential strategic partners for the equity funding of the Carolina Lithium Project, and in September 2021 we plan to apply for project debt financing from the U.S. Department of Energy’s Advanced Technology Vehicle Manufacturing Loan program. These funding processes are expected to run in parallel with our permitting/approval process.

Customer Relationships / Lithium Offtake – Piedmont maintains strong relationships with many of the leading participants in the electric vehicle supply chain, including cathode and battery manufacturers as well as automotive OEMs. The initial delivery dates contemplated in our existing spodumene concentrate sales agreement have been extended by mutual agreement.

Legal – With respect to the recent class action lawsuit filed by a Piedmont Lithium shareholder, Piedmont believes this action to be entirely without merit and we will defend ourselves vigorously.

About Piedmont Lithium

Piedmont Lithium (Nasdaq: PLL; ASX: PLL) is developing a world-class integrated lithium business in the United States, enabling the transition to a net zero world and the creation of a clean energy economy in America. Our location in the renowned Carolina Tin Spodumene Belt of North Carolina, the cradle of the lithium industry, positions us to be one of the world’s lowest cost producers of lithium hydroxide, and the most strategically located to serve the fast-growing US electric vehicle supply chain. The unique geographic proximity of our resources, production operations and prospective customers places us on the path to be the most sustainable producer of lithium hydroxide in the world and should allow Piedmont to play a pivotal role in supporting America’s move to the electrification of transportation and energy storage. For more information, please visit www.piedmontlithium.com.

Forward Looking Statements

This announcement may include forward-looking statements within the meaning of securities legislation in the United States and Australia, including statements regarding current and future plans of Piedmont and its strategic partners; strategy; value; returns; capital allocation and investment; exploration, development and construction efforts and plans; and expectations regarding permitting, production, costs and expenses. These forward-looking statements are based on Piedmont’s expectations and beliefs of Piedmont and its strategic partners concerning future events. Forward looking statements are necessarily subject to known and unknown risks, uncertainties, and other factors, many of which are outside the control of Piedmont, which could cause actual timing, achievements, results and performance to differ materially from the future timing, achievements, results and performance implied by such statements. Such factors include, among others, hazards inherent in the mining business (including risks inherent to exploring, developing, constructing and operating mining projects), risks regarding our ability to achieve profitability, enter into and deliver product under supply agreements on favorable terms, our ability to obtain sufficient financing to develop and construct our projects, our ability to comply with governmental regulations and our ability to obtain necessary permits and approvals, as well as other uncertainties and risk factors set out in filings made from time to time with the U.S. Securities and Exchange Commission and the Australian securities regulators, including, without limitation, our most recent reports on Form 10-K and Form 10-Q. Readers are cautioned not to put undue reliance on forward-looking statements. Piedmont makes no undertaking to subsequently update or revise the forward-looking statements made in this announcement, to reflect new information or the circumstances or events after the date of that this announcement.

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Resources

The Project’s Core Property Mineral Resource of 25.1Mt @ 1.13% Li2O comprises Indicated Mineral Resources of 12.5Mt @ 1.13% Li2O and Inferred Mineral Resources of 12.6Mt @ 1.04% Li2O. The Central property Mineral Resource of 2.80Mt @ 1.34% Li2O comprises Indicated Mineral Resources of 1.41Mt @ 1.38% Li2O and 1.39Mt @ 1.29% Li2O. The information contained in this announcement has been prepared in accordance with the requirements of the securities laws in effect in Australia, which differ from the requirements of U.S. securities laws. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are Australian terms defined in accordance with the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the “JORC Code”). However, these terms are not defined in Industry Guide 7 under the U.S. Securities Act of 1933, as amended (the “U.S. Securities Act”), and are normally not permitted to be used in reports and filings with the U.S. Securities and Exchange Commission (“SEC”). Effective January 1, 2021, the SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC under the U.S. Securities Exchange Act of 1934, as amended, and as a result, the SEC now recognizes estimates of “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources”. In addition, the SEC has amended its definitions of “proven mineral reserves” and “probable mineral reserves” to be “substantially similar” to the corresponding definitions under the JORC Code. However, information contained herein that describes Piedmont’s mineral deposits may not be comparable to similar information made public by U.S. companies subject to reporting and disclosure requirements under the U.S. federal securities laws and the rules and regulations thereunder. U.S. investors are urged to consider closely the disclosure in Piedmont’s Form 20-F for the fiscal year ended June 30, 2020, a copy of which may be obtained from Piedmont or from the EDGAR system on the SEC’s website at http://www.sec.gov/.

Competent Persons Statement

The information in this announcement that relates to Exploration Results, Metallurgical Testwork Results, Exploration Targets, Mineral Resources, Concentrator Process Design, Concentrator Capital Costs, Concentrator Operating Costs, Mining Engineering and Mining Schedule is extracted from the Company’s ASX announcements dated July 23, 2020, May 26, 2020, June 25, 2019, April 24, 2019, and September 6, 2018, which are available to view on the Company’s website at www.piedmontlithium.com. Piedmont confirms that: a) it is not aware of any new information or data that materially affects the information included in the original ASX announcements; b) all material assumptions and technical parameters underpinning Mineral Resources, Exploration Targets, Production Targets, and related forecast financial information derived from Production Targets included in the original ASX announcements continue to apply and have not materially changed; and c) the form and context in which the relevant Competent Persons’ findings are presented in this report have not been materially modified from the original ASX announcements.

47.0Mt @ 1.19% Li2O announced by Canada Lithium Corp. effective 12 October 2012 and available at www.sedar.com ↑

Refer to IRR’s AIM announcement dated January 28, 2020, available at www.ironridgeresources.com.au. ↑

Refer to IRR’s AIM announcement dated January 19, 2021, available at www.ironridgeresources.com.au. ↑

Reviews Project Scope and Commitment to Safety, Sustainability and Environmental Stewardship

BELMONT, N.C. – Piedmont Lithium Inc. (Nasdaq: PLL, ASX: PLL), a pre-production business targeting the integrated production of battery quality lithium hydroxide to support a US and global electric vehicle supply chain, completed its initial public presentation to the community and Board of Commissioners of Gaston County, North Carolina on July 20, 2021. The presentation addressed how the Carolina Lithium Project could position Gaston County to be a significant part of the new U.S. electric vehicle supply chain, the bipartisan support for the development of critical minerals in the United States, and Piedmont’s commitment to protect the environment and community.

“We were honored to present at last night’s meeting, and we welcomed the opportunity to provide an update on our company, our values and our proposed project to the Gaston County commissioners and our community. We confirmed last night that we would submit our North Carolina state mining permit application in August 2021 as planned, and we look forward to addressing all of the questions that arise during the permitting and rezoning process. We are committed to building the safest, most sustainable, and environmentally responsible project of this kind in the world,” said Keith Phillips, Piedmont Lithium President and CEO.

Piedmont also addressed misunderstandings in recent media reports regarding Piedmont’s development timeline, permit applications, and commitment to the environment. “Although we received important federal permits for our project in 2019, Piedmont’s upcoming state mining permit and county rezoning applications could only advance once our definitive plans were established. Our project has evolved significantly over the past four years – we have selected more efficient and environmentally friendly technology, and fully-integrated our business plan into a single campus in Gaston County, North Carolina. These project improvements have resulted in adjustments to our plans and, with the results of our recent studies and improved lithium markets, we’re excited to move forward with the state and local approval processes,” added Phillips.

About Piedmont Lithium

Piedmont is developing a world-class integrated lithium business in the United States, enabling the transition to a net zero world and the creation of a clean energy economy in America. Our location in the renowned Carolina Tin Spodumene Belt of North Carolina, positions us to be one of the world’s lowest cost producers of lithium hydroxide and the most strategically located to serve the fast-growing U.S. electric vehicle supply chain. The unique geographic proximity of our resources, production operations and prospective customers, places Piedmont on the path to be the most sustainable producer of lithium hydroxide in the world and allow Piedmont to play a pivotal role in supporting America’s move to the electrification of transportation and energy storage. Additional information is available at www.piedmontlithium.com.

Supports Piedmont’s Plan to Become America’s #1 Producer of Lithium Hydroxide

PLL to acquire 9.47% of IronRidge Resources (“IRR”) and a 50% interest in IRR’s Ghana-based lithium portfolio

$15mm equity placement and 50% project interest to be earned through staged investments over 3-4 years

Binding supply agreement for 50% of IRR’s planned Ghanaian spodumene concentrate (“SC6”) production

The IRR Ghana SC6 supply will support staged growth in Piedmont’s lithium hydroxide production

Feasibility Study of Carolina Lithium’s integrated 30,000 t/y LiOH on track for September 2021

30,000 t/y integrated LiOH project in Quebec to be evaluated jointly with Sayona Mining

IRR SC6 supply provides optionality for incremental 30,000 t/y LiOH capacity at a site to be determined

Hydroxide capacity to be developed in stages to minimize execution and funding risks

BELMONT, N.C. – Piedmont Lithium Inc. (Nasdaq: PLL) is pleased to announce that it has entered into definitive agreements (the “Agreements”) to establish a strategic partnership with IronRidge Resources (“IRR”) (AIM: IRR) through the purchase of an equity stake in IRR, staged project investments to earn a 50% interest in IRR’s Ghana-based lithium portfolio (“IRR Ghana”), and a binding supply agreement for 50% of IRR Ghana’s planned spodumene concentrate (“SC6”) production.

IRR Ghana has an impressive portfolio of spodumene prospects, anchored by the highly promising Ewoyaa Project (the “Ewoyaa Project”). The Ewoyaa Project has a current Mineral Resource of 14.5Mt @ 1.31% Li2O with vast exploration potential.[1] The Ewoyaa Project has the potential to be a large, low-cost spodumene concentrate (“SC6”) producer.

In January 2021, IRR published a scoping study for the Ewoyaa Project forecasting an average of 295,000 t/y of planned SC6 production, a $345 million after-tax net present value and an after-tax internal rate of return of 125%, for initial capital investment of $70 million.[2] The Ewoyaa Project capitalizes on its excellent location less than one mile from a major national highway and only 70 miles to the major port of Takoradi. The site is also directly adjacent to high voltage power and is expected to have a low environmental impact due to reliance on solar and hydroelectric generating capacity to power the facility. Piedmont conducted extensive due diligence over the past several months, including through site visits to Ghana, and believes that IRR Ghana has significant upside potential.

Piedmont will invest approximately $15 million (£10.8mm) to acquire a 9.47% equity interest in IRR (the “Subscription”) and will appoint one director to IRR’s Board of Directors. Piedmont will also have the opportunity to earn a 50% stake in IRR Ghana by investing (i) $17 million to fund ongoing exploration and a definitive feasibility study over the next 24 months to earn an initial 22.5% project interest, and (ii) a further $70 million in 2023-2025 to fund the construction of the Ewoyaa Project to earn an additional 27.5% project interest, which would bring the total to 50% ownership in IRR Ghana (together, the “Project Investment”). Piedmont and IRR have also entered into a binding SC6 supply agreement (the “Supply Agreement”), conditioned on Piedmont completing its earn-in obligations, pursuant to which IRR will supply Piedmont 50% of IRR Ghana’s planned SC6 production (currently estimated to be 147,500 t/y) at market prices on a life-of-mine basis.

The Subscription is expected to close in August 2021 subject to satisfaction of conditions precedent with the Project Investment expected to be staged over a three-to-four-year period leading to initial production in 2025. Material terms of the Agreements are included in the Summary of Transaction Terms at the end of this announcement.

Keith D. Phillips, President and Chief Executive Officer, commented: “We are very pleased to announce a partnership with IronRidge Resources to jointly develop their outstanding spodumene project portfolio in Ghana. We consider IRR’s Ewoyaa Project to be among the world’s most promising spodumene projects. The high-grade mineral resource is currently modest in scale but offers substantial exploration potential, and the project is very well-located, being only 70 miles from a major port. Ewoyaa builds on Piedmont’s strategic commitment to be a large-scale and low-cost producer of lithium hydroxide from spodumene concentrate sourced from diverse sustainable resources in favorable jurisdictions.

“Ghana is one of Africa’s most successful nations, with a strong mining tradition and an increasingly diverse economic base. In naming Ghana as the headquarters for its entire African business earlier this year, Twitter described Ghana as a ‘Champion for Democracy’. Euler-Hermes regularly rates Ghana among the lowest-risk jurisdictions in the region, and Transparency International rates Ghana ahead of other lithium-rich countries such as Argentina, China, Brazil, Mexico, Bolivia, Mali, and the DRC in its annual corruption perception rankings.

“2021 has been a transformative year for Piedmont. We have built the world’s premier lithium development leadership team, significantly expanded our world-class Carolina Lithium Project, and become a multi-asset company through strategic investments in Quebec and in Ghana. We raised sufficient capital in March 2021 to comfortably fund these strategic initiatives as well as our definitive feasibility study in North Carolina and should end 2021 with a robust cash balance. We will now evaluate plans to capitalize on our expanded spodumene resource base to become a larger producer of the battery-quality lithium hydroxide that America will require to power the ongoing transition to electric vehicles. Lithium has been called ‘the irreplaceable element of the electric era,’ and we will bring large-scale production of lithium hydroxide to America.”

Summary of Transaction Terms

Subscription

Subscriber

Piedmont Lithium Inc. (Nasdaq:PLL)

Issuer

IronRidge Resources (AIM:IRR)

No. of Securities

54,000,000 shares

Subscription Price

20p per share

Total Investment

£10,800,000 (approximately $15 million)

Board Representation

For so long as the Subscriber holds voting power of at least 9% in the Issuer, the Subscriber will have the right to appoint one person as a non-executive director of the Issuer

Conditions Precedent

Completion of the subscription for shares is subject to the following conditions precedent:

The Issuer obtaining shareholder approval for the issue of the shares to the Subscriber;

The Issuer and the Subscriber obtaining all necessary regulatory approvals for the subscription for shares; and

No material adverse effect on the Issuer having occurred prior to the date the other conditions precedent are satisfied.

Project Investment

Project

IronRidge Resources Ghana and its Affiliates (“IRR Ghana”)

Initial Interest

22.5% of IRR Ghana

Initial Interest Consideration

Piedmont will solely fund:

$5 million of exploration expenses

$12 million of definitive feasibility expenses

Initial Interest Condition

Piedmont’s Initial Interest will be issued upon:

Completion of definitive feasibility study

Piedmont’s election to proceed with further interest investment

Piedmont will be entitled to appoint 50% of the Board of Directors of IRR Ghana upon satisfaction of the Initial Interest Conditions

Further Interest

27.5% of IronRidge Resources Ghana and its Affiliates

Further Interest Consideration

Piedmont will solely fund the first $70 million of capital costs for the Ewoyaa Project

Further Interest Conditions

Commencement of funding of the Further Interest Consideration will occur upon:

A Decision to Mine undertaken by the Board of IRR Ghana

Customary Authorizations required for construction of the Ewoyaa Project

Other

The Parties will equally share any cost savings or overruns in the Initial or Further Interests

Customary representations, warranties, and pre-completion obligations

Conditions Precedent

The Initial and Further Interest are subject to the following Conditions Precedent

Completion of due diligence by both parties

Completion of the Share Subscription Agreement

Obtainment of all Authorizations, if any, including approval of FIRB of Australia

Market pricing (based on an average price for CIF China Price (US$) for 6.0% SC6 dry basis)

Conditions

Buyer and Seller agreeing to a start date for Product deliveries between July 2025 and July 2026 based on the development schedules of both parties

Supply Agreement is conditioned upon Piedmont’s satisfaction of earn-in obligations to acquire the Initial Interest and Further Interest of IRR Ghana

About IronRidge Resources

IronRidge Resources is an AIM-listed, Africa focused minerals exploration company with a lithium pegmatite discovery in Ghana, extensive grassroots gold portfolio in Côte d’Ivoire and a potential new gold province discovery in Chad. The Company holds legacy iron ore assets in Gabon and a bauxite resource in Australia. IronRidge’s strategy is to create and sustain shareholder value through the discovery and development of significant and globally demanded commodities. For more information, please visit www.ironridgeresources.com.au.

About Piedmont Lithium

Piedmont Lithium (Nasdaq:PLL; ASX:PLL) is developing a world-class integrated lithium business in the United States, enabling the transition to a net zero world and the creation of a clean energy economy in America. Our location in the renowned Carolina Tin Spodumene Belt of North Carolina, the cradle of the lithium industry, positions us to be one of the world’s lowest cost producers of lithium hydroxide, and the most strategically located to serve the fast-growing US electric vehicle supply chain. The unique geographic proximity of our resources, production operations and prospective customers places us on the path to be among the most sustainable producers of lithium hydroxide in the world and should allow Piedmont to play a pivotal role in supporting America’s move to the electrification of transportation and energy storage. For more information, visit www.piedmontlithium.com.

Forward Looking Statements

This announcement may include forward-looking statements. These forward-looking statements are based on Piedmont’s expectations and beliefs concerning future events. Forward looking statements are necessarily subject to risks, uncertainties and other factors, many of which are outside the control of Piedmont, which could cause actual results to differ materially from such statements. Piedmont makes no undertaking to subsequently update or revise the forward-looking statements made in this announcement, to reflect the circumstances or events after the date of that announcement. U.S. investors are urged to consider Piedmont’s disclosure in its SEC filings, copies of which may be obtained from Piedmont or from the EDGAR system on the SEC’s website at http://www.sec.gov/.

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Mineral Resources

The information contained herein and previously reported by IronRidge Resources has been prepared in accordance with the requirements of the securities laws in effect in Australia, which differ from the requirements of United States securities laws. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are Australian mining terms defined in accordance with the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (the “JORC Code”). Comparable terms are now also defined by the U.S. Securities and Exchange Commission (“SEC”) in its newly adopted Modernization of Property Disclosures for Mining Registrants as promogulated in its S-K 1300 standards. While the guidelines for reporting mineral resources, including subcategories of measured, indicated, and inferred resources, are largely similar for JORC and S-K 1300 standards, information contained herein that describes IronRidge Resources’ mineral deposits is not fully comparable to similar information made public by U.S. companies subject to reporting and disclosure requirements under the U.S. federal securities laws and the rules and regulations thereunder Piedmont does not guaranty or verify the accuracy of any disclosure made by IronRidge Resources.

Competent Persons Statements

The information in this announcement that relates to Exploration Results, Metallurgical Testwork Results, Mineral Resources, Process Design, Capital Costs, Operating Costs, Mining Engineering and Mining Schedule for Piedmont’s Carolina Lithium Project is extracted from the Company’s ASX announcements dated June 10, 2021, June 9, 2021, and April 8, 2021 which are available to view on the Company’s website at www.piedmontlithium.com. Piedmont confirms that: a) it is not aware of any new information or data that materially affects the information included in the original ASX announcements; b) all material assumptions and technical parameters underpinning Mineral Resources, Exploration Targets, Production Targets, and related forecast financial information derived from Production Targets included in the original ASX announcements continue to apply and have not materially changed; and c) the form and context in which the relevant Competent Persons’ findings are presented in this report have not been materially modified from the original ASX announcements.

Refer to IRR announcement dated January 28, 2020. ↑

Refer to IRR announcement dated January 19, 2021. ↑

Plans Underway for Large-Scale Lithium Hydroxide Production in Québec

Superior Court of Québec approves Sayona Québec’s acquisition of North American Lithium (“NAL”)

Total cash consideration of approximately C$94mm with transaction completion expected in Q3 2021

Piedmont will fund approximately C$23.5mm, representing its 25% stake in Sayona Québec

Detailed study of the integration of NAL with Sayona Québec’s Authier Project to commence in the coming weeks

Sayona and Piedmont jointly committed to development of lithium hydroxide capacity in Québec

BELMONT, N.C. – Piedmont Lithium Inc. (Nasdaq: PLL) is pleased to announce that the Superior Court of Québec (Commercial Division) has granted an approval and vesting order regarding the Company’s joint bid with Sayona Mining Limited (ASX:SYA) for the acquisition of North American Lithium (“NAL”) by Sayona Québec Inc. (“Sayona Quebec”) in the context of the Companies’ Creditors Arrangement Act (CCAA) proceedings of NAL. Piedmont is a 25% shareholder of Sayona Québec and owns 19.79% of the outstanding common shares of Sayona Mining Limited.

At the completion of the transaction Sayona Québec will acquire all the issued and outstanding shares of NAL and substantially all of its assets. The order of Superior Court of Québec provides that the assets acquired in the transaction will be free and clear of any encumbrances other than certain specific permitted encumbrances accepted by Sayona Québec.

NAL owns a large, previously-producing lithium asset project located approximately 20 miles from Sayona’s core Authier project near the important mining center of Val-d’Or in the Abitibi region of Québec. NAL is fully permitted, has a Mineral Resource of 57.7Mt @ 1.05% Li2O, and has had over $400 million invested in mining, concentrate and refining capacity. The project was operational and ramping toward nameplate production in 2018, when it was placed on care and maintenance due to weak lithium markets and a sub-optimal capital structure.

Sayona and Piedmont are proceeding with technical studies that contemplate integrating Sayona Québec’s Authier and Tansim projects with the facilities at NAL, including restart requirements, technical improvements, and optimization of NAL operations in order to fully utilize this competitive set of assets. Furthermore, Sayona and Piedmont will prioritize manufacturing of lithium hydroxide in Québec, capitalizing on Québec’s competitive advantages, including access to zero-carbon, low-cost hydropower, skilled labor, world-class infrastructure, and the initiative of both the Canadian and provincial governments to develop the lithium-ion battery materials and EV industry.

Keith D. Phillips, President and Chief Executive Officer, commented: “We are very pleased to be working with our partners at Sayona to consolidate the spodumene resources in the Abitibi region of Québec. NAL is a past-producing business with a large, high-grade mineral resource located in close proximity to Sayona’s Authier project and to the important mining center of Val-d’Or, Québec. We will work closely with Sayona to refine the plans to unify the Authier and NAL spodumene operations, and we are both committed to building integrated spodumene to lithium hydroxide capacity in Québec. Piedmont strongly believes that ‘location and regionalization of the battery supply chain matters,’ and the combined Québec operations will be well-positioned to serve the fast-growing North American electric vehicle business. The Québec operations are an ideal complement to our flagship Carolina Lithium Project in Gaston County, NC, and further Piedmont’s objective of being North America’s leading lithium hydroxide producer.”

About Piedmont Lithium Piedmont Lithium (Nasdaq:PLL; ASX:PLL) is developing a world-class integrated lithium business in the United States, enabling the transition to a net zero world and the creation of a clean energy economy in America. Our location in the renowned Carolina Tin Spodumene Belt of North Carolina, the cradle of the lithium industry, positions us to be one of the world’s lowest cost producers of lithium hydroxide, and the most strategically located to serve the fast-growing US electric vehicle supply chain. The unique geographic proximity of our resources, production operations and prospective customers places us on the path to be among the most sustainable producers of lithium hydroxide in the world and should allow Piedmont to play a pivotal role in supporting America’s move to the electrification of transportation and energy storage. For more information, visit www.piedmontlithium.com.

Forward Looking Statements This announcement may include forward-looking statements. These forward-looking statements are based on Piedmont’s expectations and beliefs concerning future events. Forward looking statements are necessarily subject to risks, uncertainties and other factors, many of which are outside the control of Piedmont, which could cause actual results to differ materially from such statements. Piedmont makes no undertaking to subsequently update or revise the forward-looking statements made in this announcement, to reflect the circumstances or events after the date of that announcement. U.S. investors are urged to consider Piedmont’s disclosure in its SEC filings, copies of which may be obtained from Piedmont or from the EDGAR system on the SEC’s website at http://www.sec.gov/.

Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Mineral Resources

The information contained herein and previously reported by North American Lithium has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are Canadian mining terms defined in accordance with the requirements of NI 43-101. Comparable terms are now also defined by the U.S. Securities and Exchange Commission (“SEC”) in its newly adopted Modernization of Property Disclosures for Mining Registrants as promogulated in its S-K 1300 standards. While the guidelines for reporting mineral resources, including subcategories of measured, indicated, and inferred resources, are largely similar for NI 43-101 and S-K 1300 standards, information contained herein that describes North American Lithium’s mineral deposits is not fully comparable to similar information made public by U.S. companies subject to reporting and disclosure requirements under the U.S. federal securities laws and the rules and regulations thereunder. Piedmont does not guaranty or verify the accuracy of any of the historical reporting of North American Lithium.

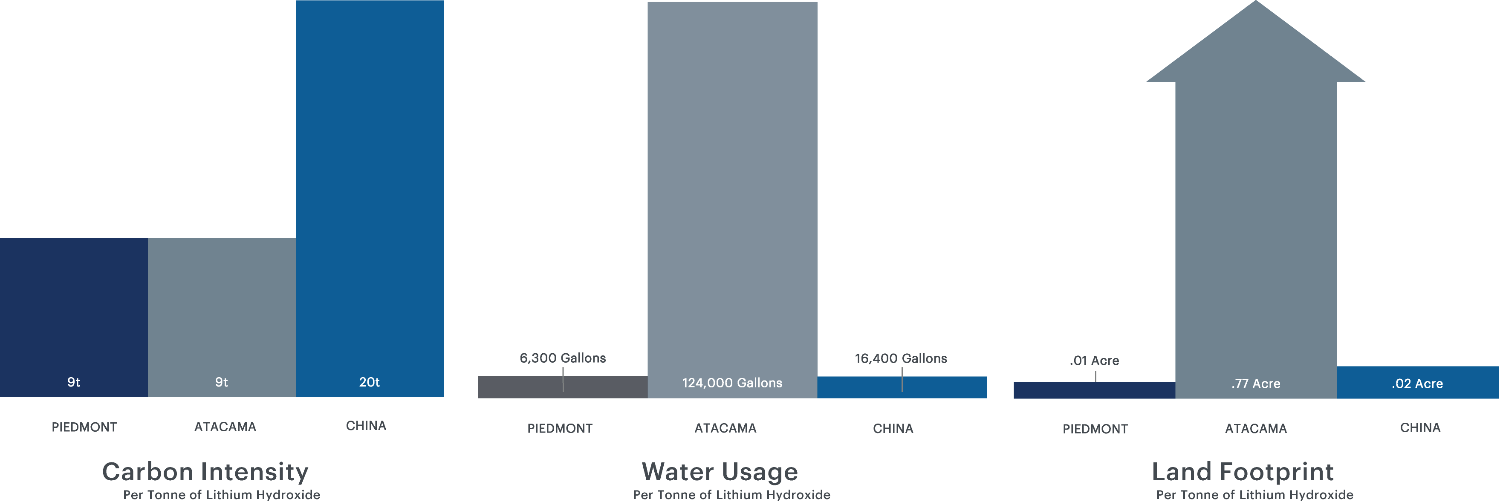

Piedmont Lithium Inc. (“Piedmont” or the “Company”) is pleased to report the results of the updated scoping study (“Scoping Study” or “Study”) for its proposed integrated lithium hydroxide business (“Carolina Lithium” or the “Project”) in Gaston County, North Carolina. The Study confirms that Carolina Lithium will be one of the world’s largest and lowest-cost producers of lithium hydroxide, with a sustainability footprint that is superior to incumbent producers, all in an ideal location to supply the rapidly growing electric vehicle supply chain in the United States.

PROJECT HIGHLIGHTS

Sustainable Lithium Hydroxide Manufacturing

Piedmont Carolina Lithium is expected to have a superior sustainability profile relative to the current producers based in China and South America. Chinese lithium producers are highly reliant on coal-fired power and generally utilize a carbon-intensive sulfuric acid roasting process to convert raw materials shipped in from Australia, while South American producers tend to utilize vast tracts of land and large quantities of water, all in the driest desert in the world, the Atacama.

Metso Outotec process reduces emissions, eliminates sulfuric acid roasting, and reduces solid waste

Solar power generation, in-pit crushing, and electric conveying reduce reliance on carbon-based energy sources

Vastly diminished transportation distances for raw materials and finished product

Highly efficient land and water use compared with South American brine production

Far lower CO2 intensity than incumbent China hydroxide production including Scope 1, 2, and 3 emissions

Independent preliminary Life-Cycle Analysis (“LCA”) completed with Minviro

Figure 1 – Life cycle analysis of key carbon intensity, water usage, and land footprint of Piedmont Carolina Lithium

Exceptional Economics and Scale

The Study confirms that Piedmont will be a large and low-cost producer of lithium hydroxide, benefitting from its ideal location in Gaston County, North Carolina, with exceptional infrastructure, a deep local talent pool, low-cost energy, and proximity to local markets for the monetization of by-product industrial minerals. The Study results represent a substantial improvement over prior studies despite the use of more conservative assumptions related to mining dilution and metallurgical recoveries.

The competitive advantage of Piedmont’s unique location is depicted in the following lithium hydroxide cost curve, which was prepared by Roskill, a leading lithium industry consultancy.

Figure 2 – Lithium hydroxide 2028 AISC cost curve (real basis) (Roskill) AISC includes all direct and indirect operating costs including feedstock costs (internal AISC), refining, corporate G&A and selling expenses.

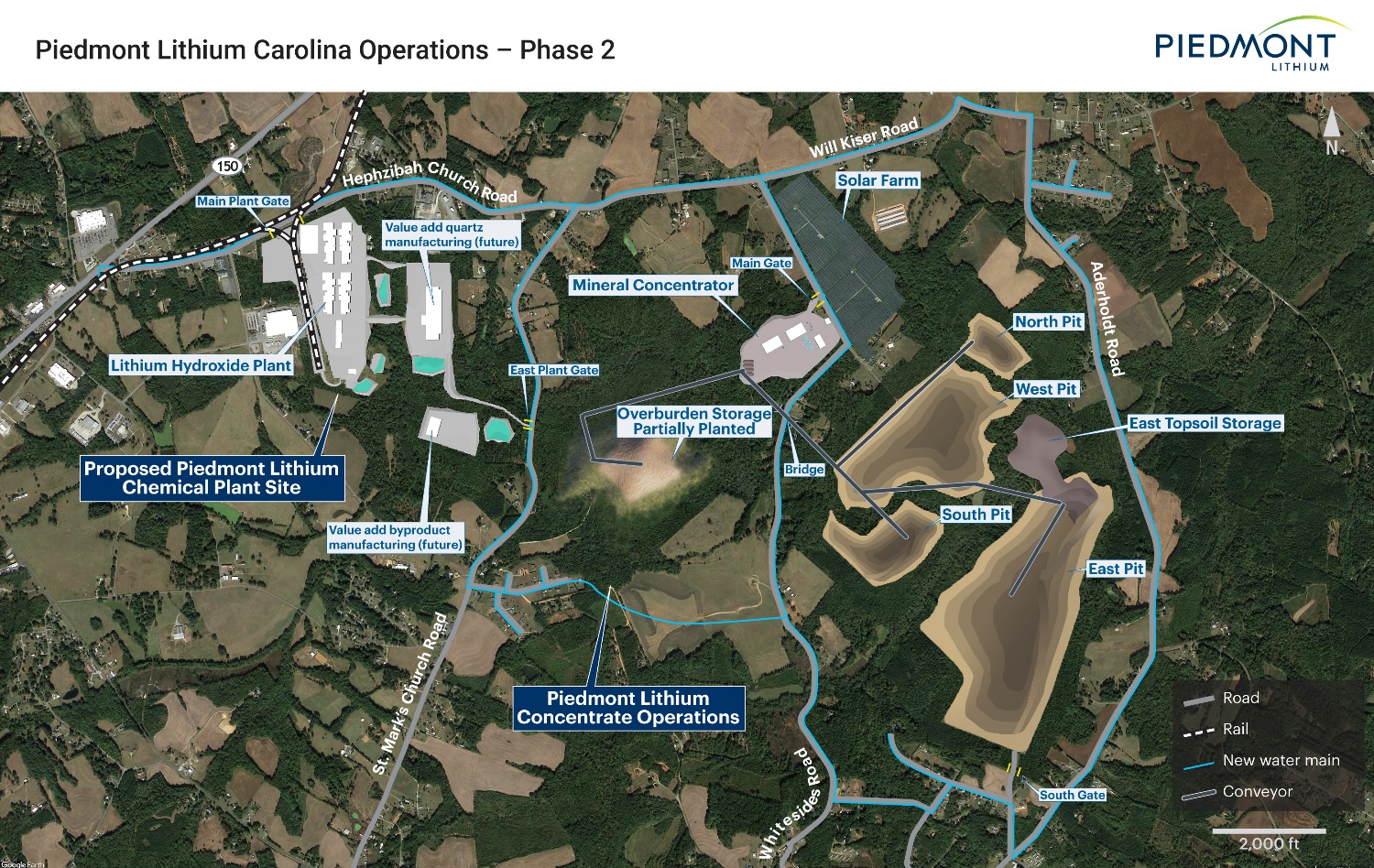

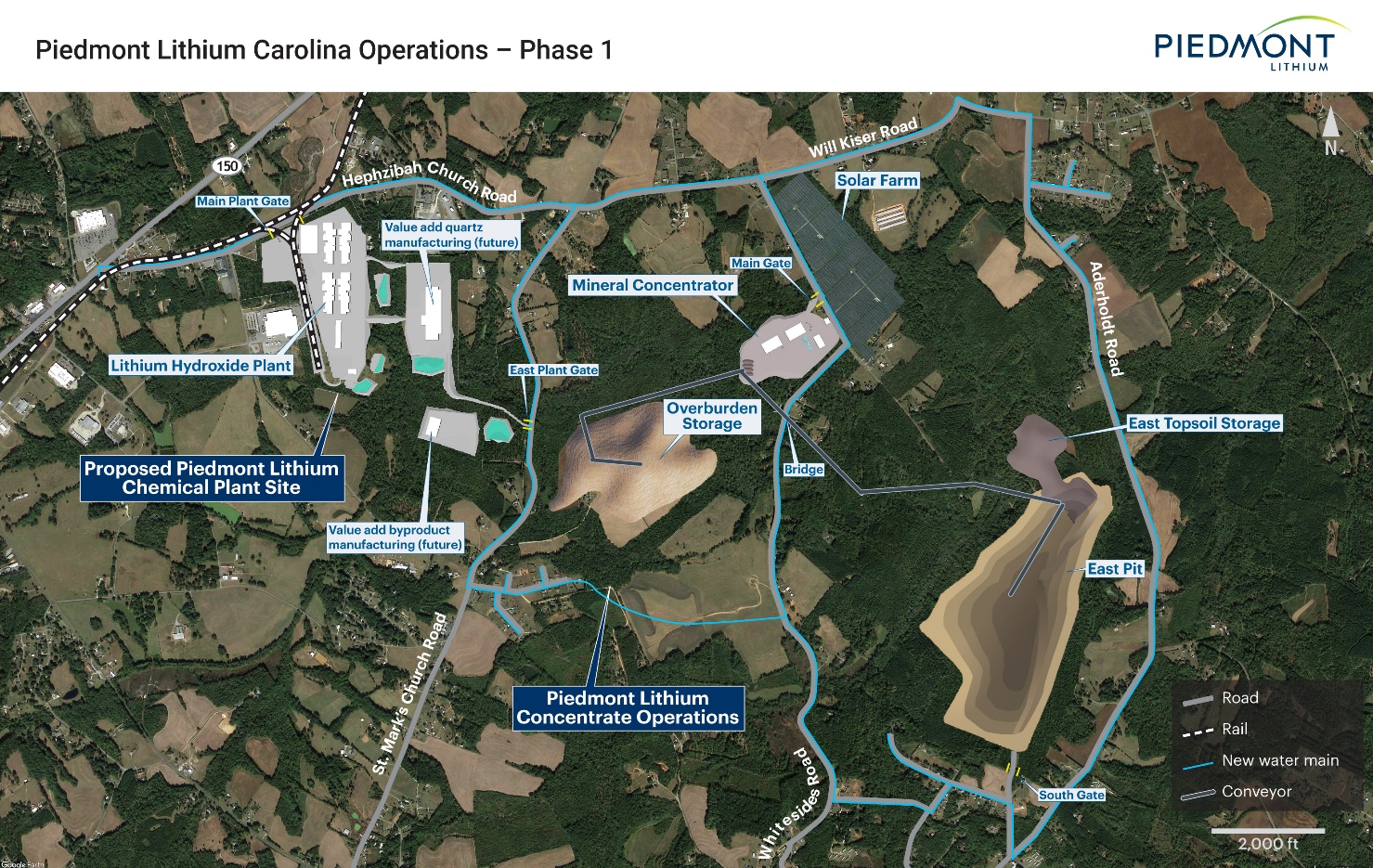

Fully Integrated Manufacturing Campus

Piedmont Carolina Lithium contemplates a single, integrated site, comprising quarrying, spodumene concentration, by-products processing, and spodumene conversion to lithium hydroxide. There are currently no such integrated sites operating anywhere in the world, and the economic and environmental advantages of this strategy are compelling:

Premier location in Gaston County, North Carolina – “the cradle of the lithium business”

Elimination of SC6 transportation costs and related noise and emissions

On-site solar complex to power concentrate operations and reduce reliance on diesel fueled equipment

Potential to co-locate other downstream battery materials / Li-ion battery manufacturing

Creation of up to 500 manufacturing, engineering, and management jobs

Site offers potential to expand hydroxide capacity by adding additional manufacturing trains in the future

Figure 3 – Indicative proposed site plan for Piedmont’s Carolina Lithium operations

“We are exceedingly pleased with the results of our updated Scoping Study. The economics of our Project continue to impress, but I am particularly proud of the Project’s sustainability profile. Customers, investors, and neighbors are increasingly focused on businesses that are “doing things the right way.” It is critical that raw material supply chains do not detract from the overall sustainability of the transition to electric vehicles. Our project will have a far lower environmental footprint than alternative suppliers, and we expect that to position Piedmont well with all stakeholders.

As we move forward to complete a Definitive Feasibility Study for Carolina Lithium later in 2021, Piedmont has engaged Evercore and JPMorgan as financial advisors to evaluate potential strategic partnering and financing options for its North Carolina Project. Given the Project’s unique position as the only American spodumene project, with world-class scale, economics, and sustainability, we expect strategic interest to be robust.

Keith D. Phillips, President and Chief Executive Officer

scoping study update

Piedmont’s Carolina Lithium Scoping Study Update is based on the Company’s Mineral Resource estimate reported in April 2021, of 39.2 Mt at a grade of 1.09% Li2O and the by-product Mineral Resource estimates comprising 7.4 Mt of quartz, 11.1 Mt of feldspar and 1.1 Mt of mica reported in June 2021.

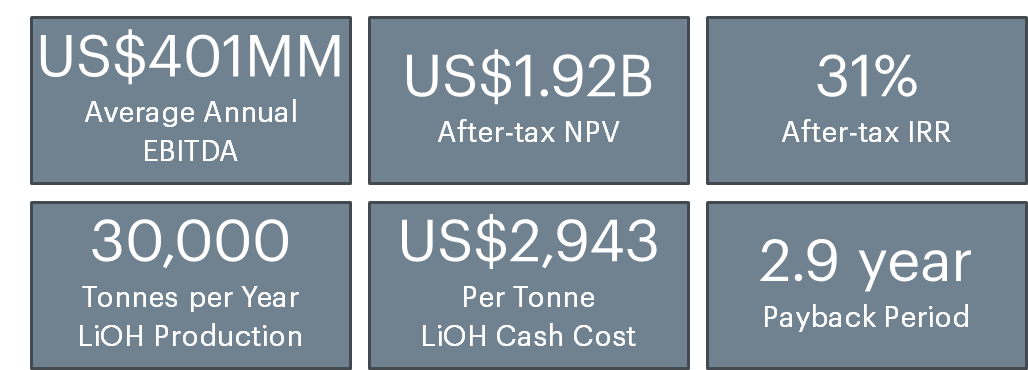

The fully integrated Study contemplates a 20-year project life, with the downstream lithium hydroxide chemical plant commencing 90 days after the start of concentrate operations. The chemical plant is assumed to achieve full capacity within 12 months. Table 1 provides a summary of production and cost figures for the integrated Project.

Table 1: Project Summary Outcomes

Unit

Estimated Value

Annual Production

Operation life

years

20

Steady state annual lithium hydroxide production

t/y

30,000

Average annual spodumene concentrate (SC6) production

t/y

248,000

Average annual quartz production

t/y

252,000

Average annual feldspar production

t/y

392,000

Average annual mica production

t/y

70,000

Life-of-Mine (“LOM”) Production

Production target

Mt

37.41

LOM SC6 production

Mt

4.96

LOM quartz production

Mt

4.83

LOM feldspar production

Mt

7.51

LOM mica production

Mt

1.34

LOM feed grade (excluding dilution)

%

1.09

LOM average concentrate grade

%

6.0

LOM average process recovery

%

80

LOM average strip ratio

waste:ore

12.2:1

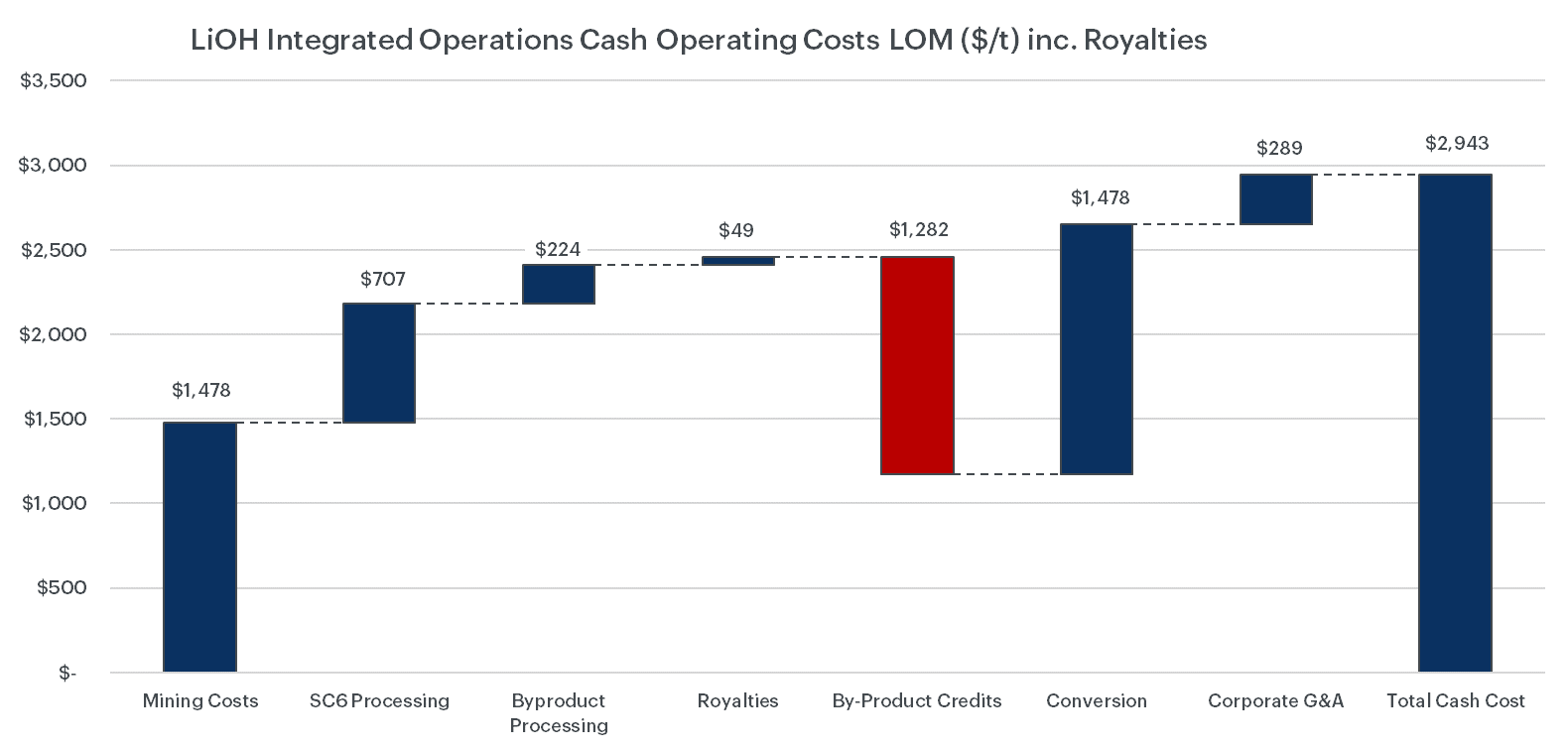

Operating and Capital Costs

Average LiOH production cash costs

US$/t

$2,943

Average LiOH production all in sustaining costs

US$/t

$3,145

Direct development capital

US$MM

$639.0

Land acquisition costs

US$MM

$28.0

Other owner’s costs

US$MM

$43.8

Contingency

US$MM

$127.8

Total initial capital cost

US$MM

$838.6

Sustaining and deferred capital

US$MM

$337.9

Working capital

US$MM

$48.3

Financial Performance

Average annual steady state EBITDA

US$MM/y

$401

Average annual steady state after-tax cash flow

US$MM/y

$315

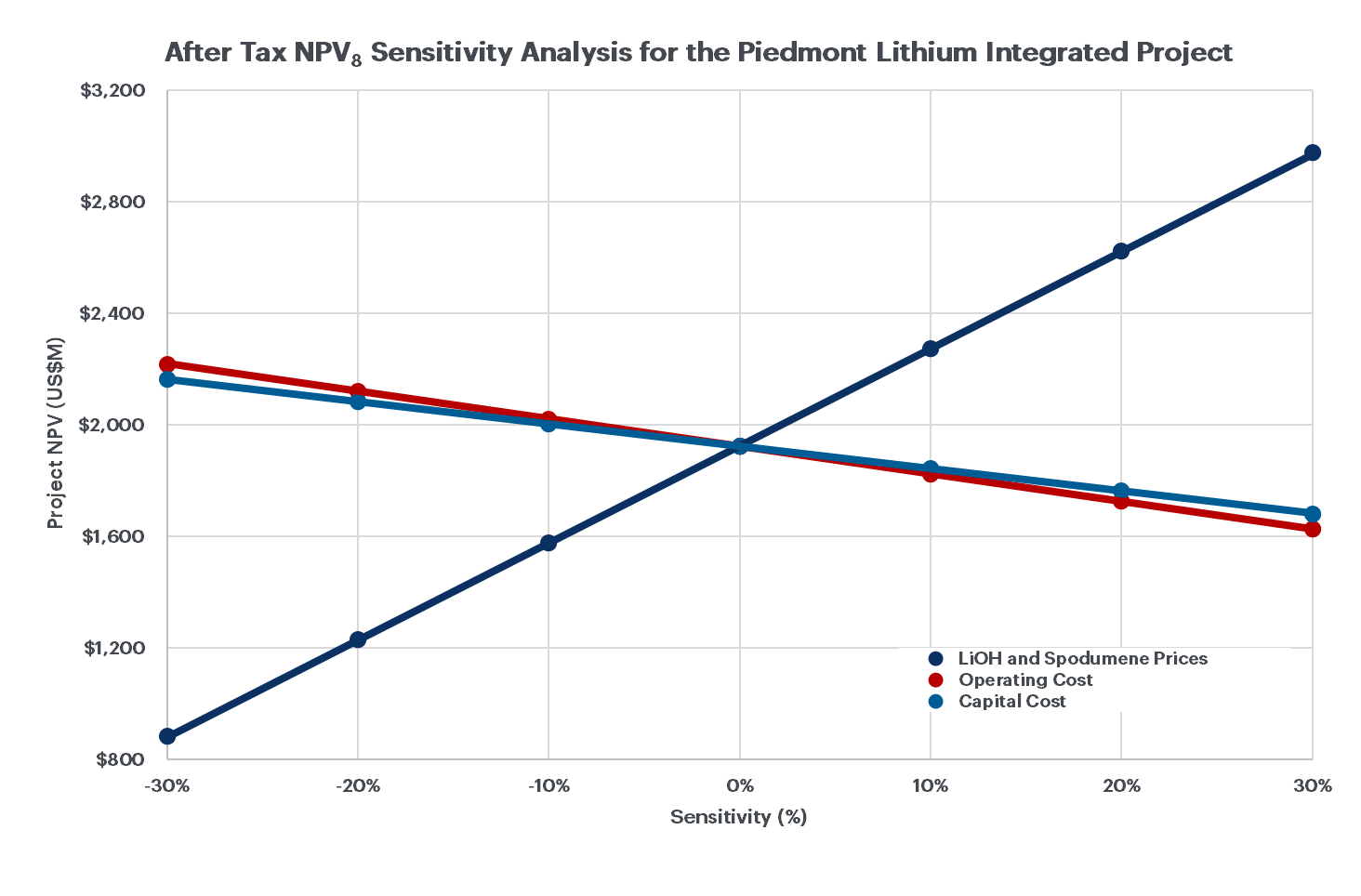

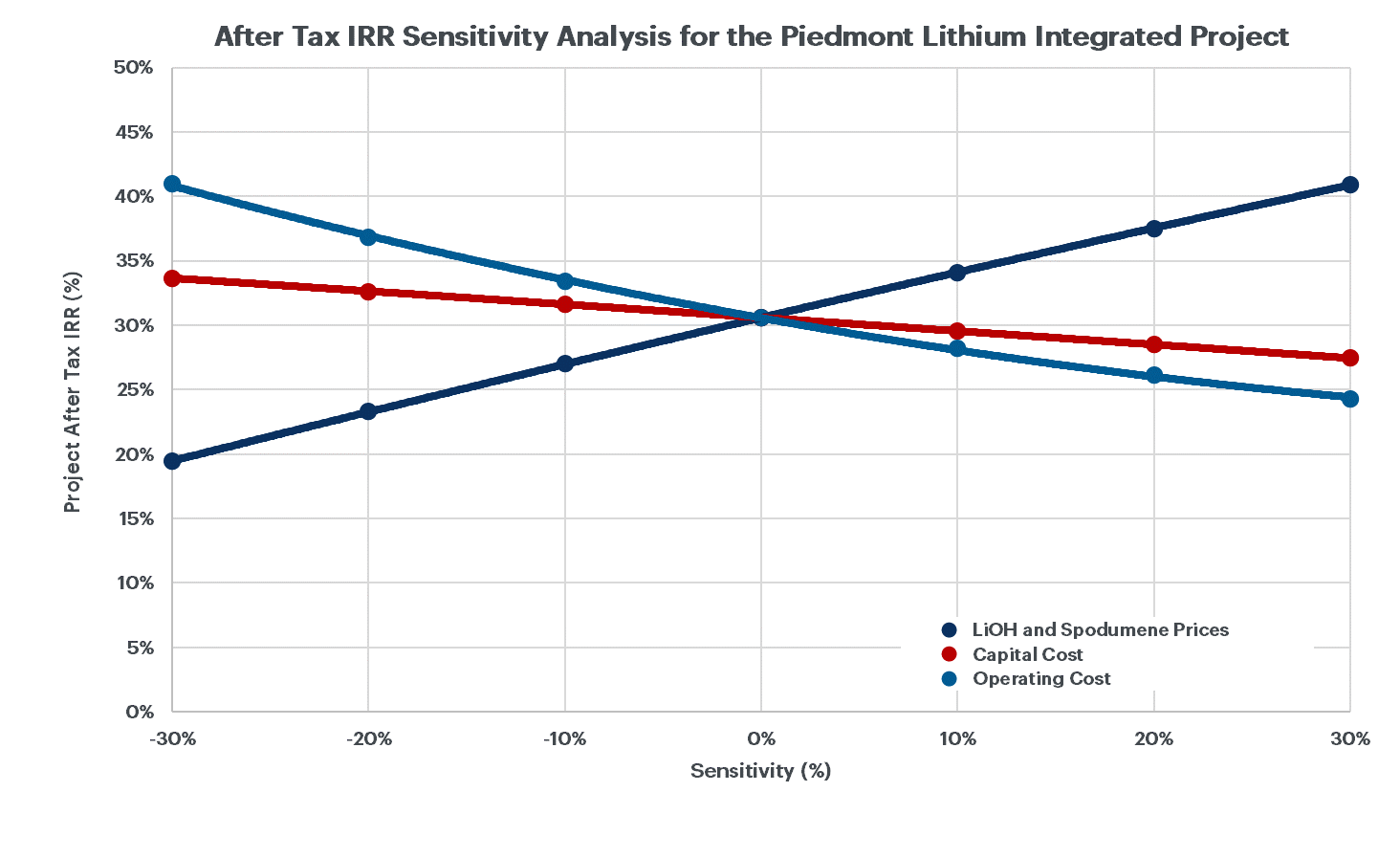

After tax Net Present Value (“NPV”) @ 8% discount rate

US$MM

$1,923

After tax Internal Rate of Return (“IRR”)

%

31%

Payback from start of operations

years

2.9

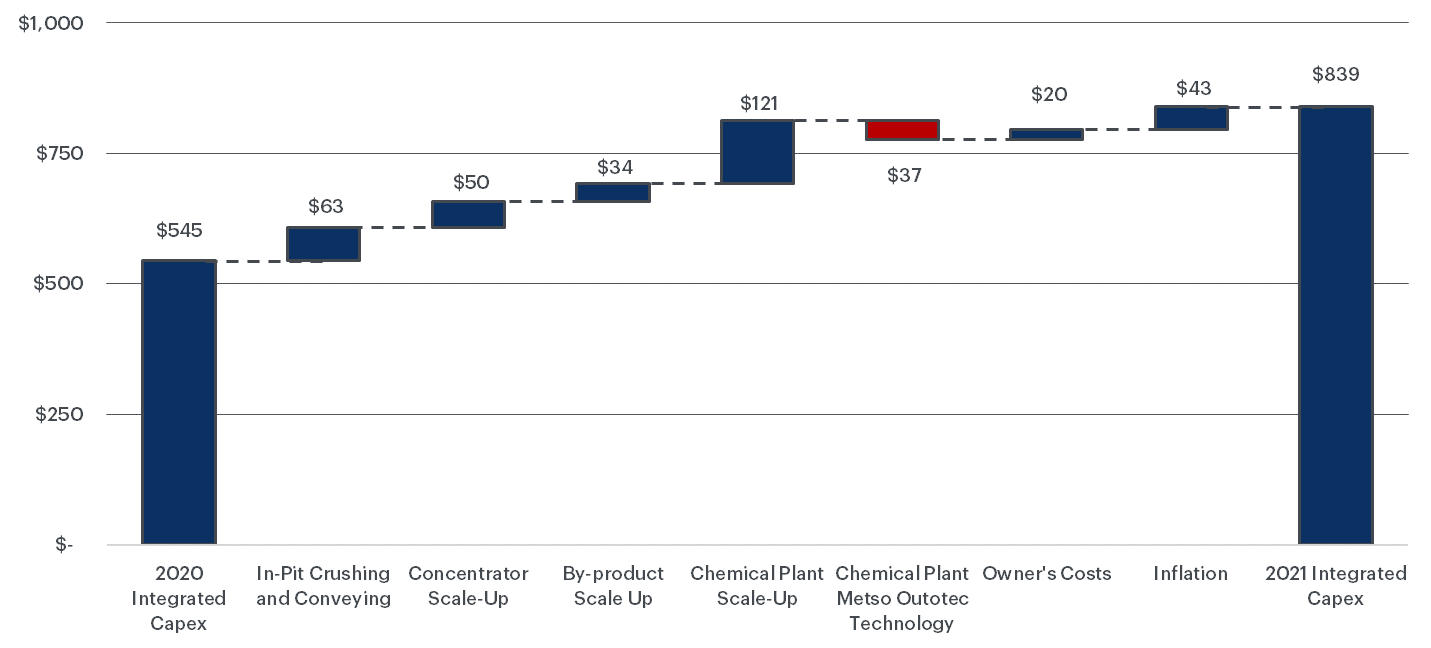

Updates from Prior Studies

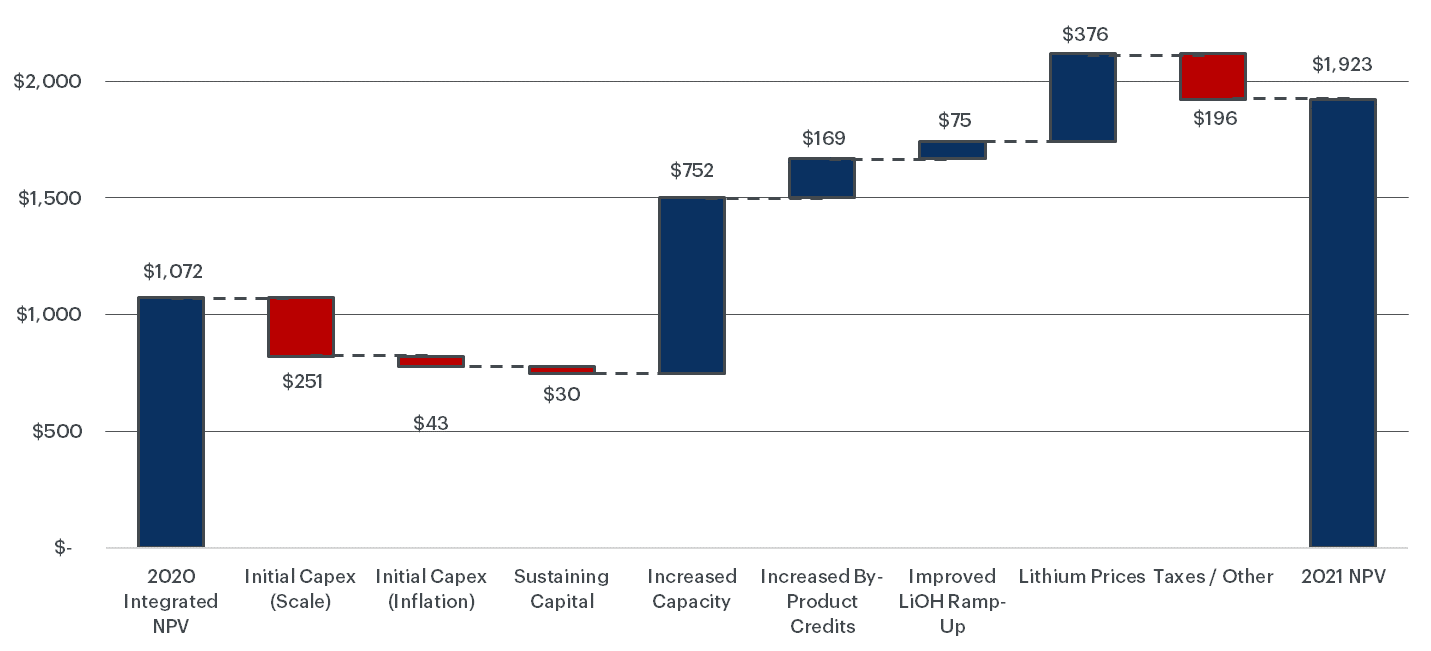

Notable improvements to business outcomes have been achieved in this Study compared with the prior scoping study published in May 2020. Key updates are reflected in Table 2.

Table 2: Comparative Outcomes of 2021 and 2020 Scoping Studies

Outcomes

Unit

2021 Study

2020 Study

Project life

years

20

25

Steady-state average annual lithium hydroxide production

t/y

30,000

22,720

Steady-state average annual spodumene concentrate production

t/y

248,000

160,000

Steady-state average annual by-product production (all products)

t/y

714,000

224,000

Long term lithium hydroxide price

US$/t

$15,239

$12,910

Long term spodumene concentrate price

US$/t

$762

$564

Steady-state average cash cost of lithium hydroxide production

US$/t

$2,943

$3,712

Steady-state average cost of spodumene concentrate production

US$/t

$181

$201

Initial capital cost (including contingency)

US$MM

$838

$545

Steady-state average annual EBITDA

US$MM/y

$401

$218

After tax NPV @ 8% discount rate

US$MM

$1,923

$1,071

After tax IRR

%

31%

26%

Payback from start of operations

years

2.92

3.23

Figure 4 shows the impact of key project changes to Project NPV.

Figure 4 – Updated economic model impact to NPV8 on the Carolina Lithium Project (US$ Billion)

These improved results for the proposed operations have been achieved based on changes to the project design:

Production values have been modified

Run-of-mine ore production increased to 1.95Mt/y from 1.15 Mt/y

SC6 production increased to 248,000 t/y from 160,000 t/y

LiOH production increased to 30,000 t/y from 22,720 t/y

Quartz production increased to 252,000 t/y from 86,000 t/y

Feldspar production increased to 392,000 t/y from 125,000 t/y

Mica production increased to 70,000 t/y from 13,000 t/y

Product pricing has been updated to 2021 long-term forecasts for LiOH, SC6, and by-products

Environment, Sustainability, and Governance

Over the past year, the Company has taken steps to improve upon the advantages present in North Carolina. Minviro, an industry-leading practitioner of Life Cycle Assessment (LCA) impacts of manufacturing battery materials was engaged by Piedmont to complete a prospective LCA of the integrated lithium hydroxide operations. Together with Minviro, Piedmont has enhanced our sustainability footprint by implementing the following initiatives in our Study update:

Working with a solar developer to build and operate a solar farm on Piedmont property capable of producing electricity to supply up to 100% of Piedmont needs

Utilizing electric equipment to the greatest extent possible including transporting ore from pit operations to the concentrator to reduce fossil fuel consumption

Co-locating all operations on the same proposed site in Gaston County minimizing any transit and allowing unused by-products streams to be repurposed for site redevelopment

Expanding the by-products operations to serve valuable markets for quartz, feldspar and mica

Minviro worked with Piedmont to identify areas for improvement in operations on a cradle-to-gate basis using the work that Piedmont completed in prior studies. Piedmont is now setting a target to produce lithium hydroxide with a carbon intensity of less than 9 kg of CO2-e/Kg of lithium hydroxide including complete Scope 1, 2 and upstream Scope 3 emissions. This target is nearly half of the carbon intensity of incumbent producers of lithium hydroxide starting with spodumene mined in Western Australia and chemically refined in China. It is on par with brine-based production routes to lithium hydroxide which require considerable quantities of reagents to be transported by ocean going vessels and supplies of fresh water in a water scarce region.

Scoping Study Consultants

This Scoping Study update combines information and assumptions provided by a range of independent consultants, including the following consultants who have contributed to key components of the Study.

Table 3: Scoping Study Consultants

Consultant

Scope of Work

Primero Group Limited

Concentrate operations and overall Study integration

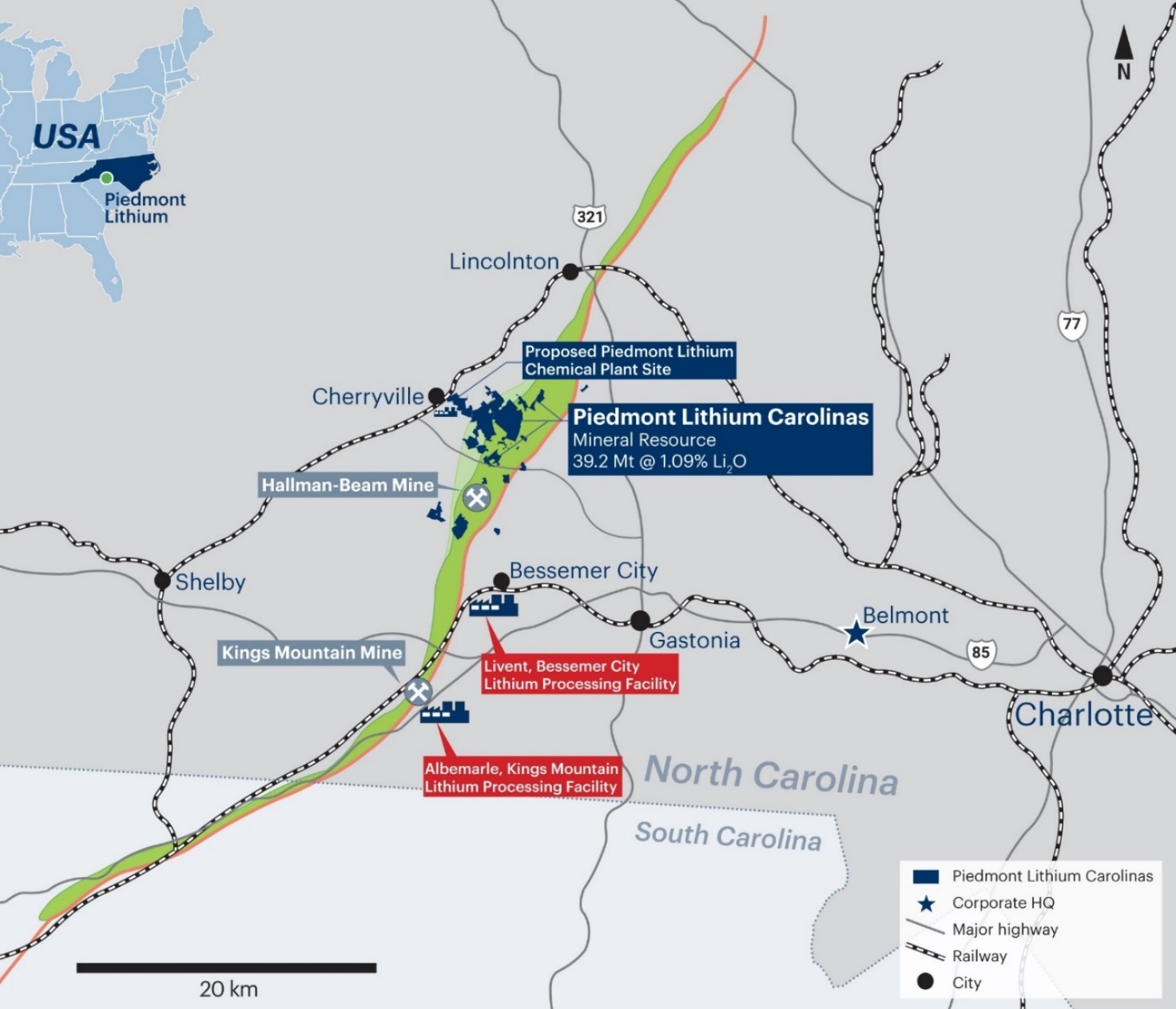

Piedmont holds a 100% interest in the Carolina Lithium Project located within the Carolina Tin-Spodumene Belt (“TSB”) and along trend to the Hallman Beam and Kings Mountain mines, which historically provided most of the western world’s lithium between the 1950s and the 1980s. The TSB has been described as one of the largest hard rock lithium regions in the world and is located approximately 25 miles west of Charlotte, North Carolina.

The Company has reported Mineral Resource estimates (“MRE”) for the Project. Piedmont has completed 495 drill holes on these properties totaling 82,924 meters to date spanning four drill campaigns.

As of March 31, 2021, the Project comprised approximately 2,667 acres of surface property and associated mineral rights, of which approximately 988 acres are owned, approximately 113 acres are subject to long-term lease, approximately 79 acres are subject to lease-to-own agreements, and approximately 1,487 acres are subject to exclusive option agreements. These exclusive option agreements, upon exercise, allows Piedmont to purchase or, in some cases, enter into long-term lease agreements for the surface property and associated mineral rights.

Figure 5 – Piedmont’s location within the TSB

Mineral Resource Estimates

On April 8, 2021 the Company announced an updated MRE prepared by independent consultant McGarry Geoconsulting Corp. (“McGarry Geo”) in accordance with JORC Code (2012 Edition). The total lithium Mineral Resources reported by Piedmont for the Carolina Lithium Project are 39.2 Mt grading at 1.09% Li2O.

Table 4: Piedmont Carolina Lithium Mineral Resources Estimate

Resource Category

Tonnes

(Mt)

Grade

(Li2O%)

Li2O

(t)

LCE

(t)

Indicated

21.6

1.12

241,000

597,000

Inferred

17.6

1.03

181,000

449,000

Total

39.2

1.09

422,000

1,046,000

On June 8, 2021 the Company announced updated MREs for by-products quartz, feldspar, and mica. The results are shown in Table 5. The by-product MRE’s have been prepared by independent consultants, McGarry Geo and are reported in accordance with the JORC Code (2012 Edition). The economic extraction of by-product minerals is contingent on Piedmont’s economic extraction of lithium Mineral Resources. Accordingly, the by-product Mineral Resource estimates are reported at a 0.4% Li2O cut-off grade, consistent with the reported lithium MRE.

Table 5: Mineral Resource Estimates – By-product Minerals

Category

Tonnes (Mt)

Li2O

Quartz

Feldspar

Mica

Grade (%)

Tonnes (t)

Grade (%)

Tonnes (Mt)

Grade (%)

Tonnes (Mt)

Grade (%)

Tonnes (Mt)

Indicated

21.6

1.12

241,000

29.4

6.34

45.0

9.69

4.2

0.90

Inferred

17.6

1.03

181,000

29.3

5.16

45.9

8.08

4.1

0.73

Total

39.2

1.09

422,000

29.4

11.50

45.4

17.77

4.2

1.63

Production Target

Pit optimizations were completed by Marshall Miller in order to produce a production schedule on an annual basis. This resulted in a total production target of approximately 4.96 Mt of 6.0% Li2O spodumene concentrate (“SC6”), averaging approximately 248,000 t/y of SC6 over the 20-year mine life. This equates to an average of 1.95 Mt/y of ore processed, totaling approximately 37.4 Mt of run-of-mine (“ROM”) ore at an average ROM grade of 1.09% Li2O (undiluted) over the 20-year mine life.

The Study assumes concentrate operations and chemical plant operations production life of 20 years, commencing in year 1 of the Project. It is assumed that concentrate operations including by-products will commence about 90 days in advance of chemical plant start-up to build initial SC6 inventory. SC6 produced in excess of chemical plant requirements are assumed to be sold to third parties during the life of the Project. Of the total production target of 4.96 Mt of SC6, approximately 1.19 Mt will be sold to third parties during the operational life and approximately 3.77 Mt will be supplied to Piedmont’s chemical plant operations for conversion into lithium hydroxide, resulting in a total production target of approximately 582,000 t of lithium hydroxide, averaging approximately 29,095 t/y of lithium hydroxide over the 20-year production life.

Of the 582,000 t lithium hydroxide production target 567,000 t are expected to be sold as battery-grade quality lithium hydroxide with 15,000 t sold as technical-grade quality based on the estimated ramp-up of the lithium chemical plant.

The Study assumes production targets of 4.83 Mt of quartz concentrate, 7.51 Mt of feldspar concentrate, and 1.34 Mt of mica concentrate over the life of operations based on the potential recovery of these products from the concentrator flotation circuits and the Company’s analysis of domestic industrial minerals markets and engagement with prospective customers.

There remains significant opportunity to increase the operational life of Carolina Lithium beyond 20 years by discovery of additional resources within the TSB within a reasonable trucking or conveying distance to the proposed concentrator.

Mining

Independent consultants Marshall Miller and Associates used SimSched™ software to generate a series of economic pit shells using the updated Mineral Resource block model and input parameters as agreed by Piedmont. Overall slope angles in rock were estimated following a preliminary geotechnical analysis that utilized fracture orientation data from oriented core and downhole geophysics (Acoustic Televiewer), as well as laboratory analysis of intact rock strength. The preliminary geotechnical assessment involved both kinematic and overall slope analyses utilizing Rocscience™ modeling software.

Overall slope angles of 45 degrees were assumed for overburden and oxide material. Overall slope angles of 53 degrees were estimated for fresh material which includes a ramp width of 30 meters. Production schedules were prepared for the Project based on the following parameters:

A targeted run-of-mine production of 1.95 Mt/y targeting concentrator output of about 248,000 t/y of SC6

Mining dilution of 10%

Mine recovery of 100%

Concentrator processing recovery of 80%

Mine sequence targets maximized utilization of Indicated Mineral Resources at the front end of the schedule

The results reported are based upon a scenario which maximizes extraction of Indicated Resources in the early years of production. Indicated resources represent 100% of the tonnes processed in years 1-3 of operations. The results reported assume that the Core property is mined from year 1-17 with the Central property mined in years 17-19 and the Huffstetler property mined in years 19-20. Table 6 shows the production target.

Table 6: Total Production Target for Piedmont Properties

Property

ROM Tonnes Processed

(kt)

Waste Tonnes Mined

(kt)

Stripping Ratio

(W:O t:t)

ROM Li2O Diluted Grade

(% )

Production Years

Tonnes of SC6

(kt)

Core

30,593

378,603

12.4

0.99

1-17

4,050

Central

4,251

49,467

11.6

1.12

17-19

632

Huffstetler

2,564

28,511

11.1

0.81

19-20

278

Total

37,408

456,581

12.2

0.99

1-20

4,960

Concentrate Metallurgy

Piedmont engaged SGS Canada Inc. in Lakefield, Ontario to undertake testwork on variability and composite samples. Dense Medium Separation (“DMS”) and locked-cycle flotation tests produced high-quality spodumene concentrate with a grade above 6.0% Li2O, iron oxide below 1.0%, and low impurities from composite samples. Table 7 shows the results of composite tests on the preferred flowsheet which were previously announced on July 17, 2019. The feed grade of the composite sample was 1.11% Li2O.

This Study assumes a spodumene recovery of 80% when targeting a 6.0% Li2O spodumene concentrate product. The Company is currently undertaking additional variability sample testing concurrent with ongoing Definitive Feasibility Study (“DFS”) activities.

Table 7: Dense Medium Separation and Locked Cycle Flotation Test Concentrate Assays

Sample

Li2O

(%)

Fe2O3

(%)

Na2O

(%)

K2O

(%)

CaO+ MgO + MnO (%)

P2O5

(%)

Dense medium separation

6.42

0.97

0.56

0.45

0.51

0.12

Locked-cycle flotation

6.31

0.90

0.68

0.52

1.25

0.46

Combined concentrate

6.35

0.93

0.63

0.49

0.96

0.32

By-Product Metallurgy

The production of bulk quartz and feldspar concentrates as by-products from the spodumene locked-cycle flotation tailings was investigated. Six individual batch tests were conducted with the quartz and feldspar concentrates being composited. The results of these tests are provided in Table 8 (results previously announced May 13, 2020). Additional by-product testwork in conjunction with DFS is ongoing.

Piedmont engaged North Carolina State University’s Minerals Research Laboratory in 2018 to conduct bench-scale testwork on samples obtained from the Company’s MRE within the Core Property for by-products quartz, feldspar, and mica. The objective of the testwork program was to develop optimized conditions for spodumene flotation and magnetic separation for both grade and recovery. Summary mica concentrate data are shown in Table 9. Complete mica data were previously announced on September 4, 2018. Further mica product optimization is in progress in conjunction with the DFS.

Mica quality is measured by its physical properties including bulk density, grit, color/brightness, and particle size. The bulk density of mica by-product generated from Piedmont composite samples was in the range of 0.680 – 0.682 g/cm3.

The National Gypsum Grit test is used mostly for minus 100 mesh mica which issued as joint cement compound and textured mica paint. Piedmont sample grit results were in the range of 0.70 – 0.79%, well below the typical specification for total grit in mica of 1.0%. Color/brightness is usually determined on minus 100 mesh material. Several instruments are used for this determination including the Hunter meter, Technedyne and the Photovoltmeter. The green reflectance is often reported for micas and talcs. Piedmont Green Reflectance results were in the range of 11.2 – 11.6.

Process Design

The concentrator process design is based on prior SGS testwork. Flowsheet optimization is ongoing with a variability testwork program at SGS in conjunction with the Company’s definitive feasibility study. Lithium hydroxide manufacturing process design is based on Metso Outotec experience. A pilot-scale testwork program is currently underway to confirm process design as part of the Company’s ongoing definitive feasibility study.

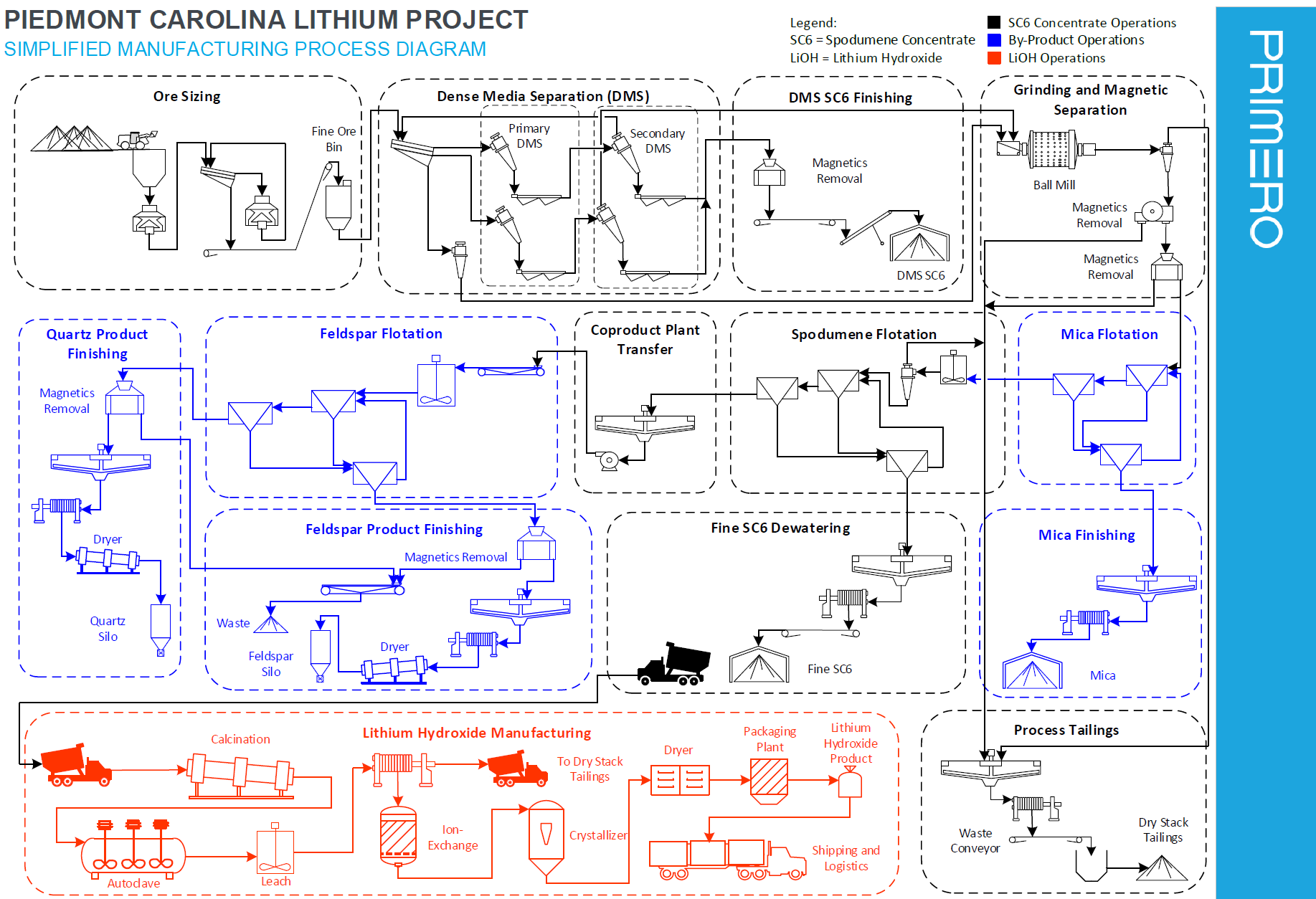

The simplified process flow diagram for the Project is shown in Figure 6.

A preliminary integrated site plan including mining operations, concentrate operations, lithium hydroxide manufacturing, overburden and waste rock disposal, by-product manufacturing and ancillary facilities was developed by Marshall Miller and Primero Group during the course of study. Figure 7 shows the indicative site plan for the proposed integrated manufacturing campus.

Figure 7 – Proposed integrated manufacturing campus site plan

Infrastructure

Piedmont enjoys a superior infrastructure position relative to most lithium projects globally. The proposed site is approximately 25 miles west of Charlotte, North Carolina. The site is directly accessible by multiple state highways, CSX railroad, and is in close proximity to U.S. Highway 321 and U.S. Interstate I-85.

Piedmont’s proposed Carolina Lithium operations are in proximity to four (4) major US ports:

Charleston, SC – 197 miles

Wilmington, NC – 208 miles

Savannah, GA – 226 miles

Norfolk, VA – 296 miles

Charlotte-Douglas International Airport is 20 miles from the proposed operations. Charlotte-Douglas is the 6th largest airport in the United States and has direct international routes to Canada, the Caribbean, South America, and Europe.

Temporary or permanent camp facilities will not be required as part of the Project. Furthermore, Livent Corporation and Albemarle Corporation operate lithium chemical plants in close proximity to the proposed Piedmont operations, and the local region is well serviced by fabrication, maintenance, and technical service contractors experienced in the sector.

Logistics

Most spodumene concentrate produced by Piedmont will be consumed by the Piedmont Carolina Lithium chemical plant. For internal transportation costs within the integrated campus a US$2.00/t cost is included in the financial model for the internal site transport between the concentrate operations and chemical plant.

Permitting

HDR Engineering has been retained by Piedmont to support permitting activities on the proposed Project.

In November 2019, the Company received a Clean Water Act Section 404 Standard Individual Permit from the US Army Corps of Engineers for the concentrate operations. This is the only federal permit required for the concentrate operations. The Company has also received a Section 401 Individual Water Quality Certification from the North Carolina Division of Water Resources.

The concentrate operations require a North Carolina State Mining Permit from the North Carolina Department of Environmental Quality (“NCDEQ”) Division of Energy, Mineral and Land Resources. A permit application is well advanced and will be submitted to North Carolina following additional pre-application consultation over the coming months.

Piedmont previously received a Clean Air Act Title V synthetic minor permit from the NCDEQ Division of Air Quality for a proposed lithium hydroxide operation in Kings Mountain. Piedmont will apply for a new Title V synthetic minor air permit for the proposed Gaston County chemical plant location in the coming months.

The overall proposed integrated Project remains subject to conditional district rezoning within Gaston County. A rezoning application will proceed following additional pre-application consultation with Gaston County and community leaders following publication of the Study results.

Marketing

Lithium Market Outlook

Benchmark Mineral Intelligence (“Benchmark”) reports that total battery demand will grow to 312 GWh in 2021 translating to 297kt of LCE demand in 2021, a growth of 41% over 2020 demand. Benchmark forecasts total demand in 2021 to be 430kt on an LCE basis.